A study by Engprax found that projects with clear upfront requirements were 97% more likely to succeed. In financial services, unclear requirements carry a second cost that project managers rarely track. When the wrong things get scoped at the start, the problems show up in examinations and integration failures.

Before you scope a custom financial software build, get three things straight:

The financial institutions that get custom software right follow a simple pattern. They only build custom where it actually matters: how compliance logic connects to transaction data, who controls the integration layer, and how AI decisions get documented. Everything else? They use standard platforms.

The ones that struggle, try to build everything custom. They spend a budget on account management workflows that any standard platform handles fine. And then they run out of time and money before they get to the parts that actually need custom work, the compliance architecture, the data ownership layer, the AI governance.

With the ability to customize the software to fit their operational workflows, business models, and customer expectations, organizations can ensure that their systems evolve alongside industry trends, regulations, and technological advances.

Also Read: Top Benefits of Custom Software Development for Business Growth

While off-the-shelf solutions are ready-made and cost-effective, they often come with limitations in functionality and scalability, making them unsuitable for businesses with specialized needs. Custom financial software, on the other hand, is designed to effortlessly align with an organization’s existing processes and systems.

Some key differences include:

Here's how custom financial software compares to off-the-shelf tools when it comes to security, compliance, flexibility, and long-term value.

With rising data privacy regulations, increasing need for scalability, and evolving customer expectations, financial institutions are accelerating digital transformation-investing in flexible, modular, and scalable technology platforms that go beyond rigid, one-size-fits-all tools.

Not sure if custom financial software is right for your organization? Speak with our financial technology architects to get a tailored feasibility assessment.

As financial services evolve, the demand for personalized, secure, and scalable solutions is more critical than ever. Custom financial software development allows organizations to stay competitive by aligning technology with business goals, enhancing security, and ensuring regulatory compliance.

Every financial institution operates differently, with unique business processes, customer demands, and regulatory obligations. Custom financial software is designed to fit these specific needs, unlike generic solutions that offer one-size-fits-all features.

Whether it's a complex loan management system or a personalized investment platform, custom software is built to align with your workflows, ensuring that the technology supports your goals and objectives, not the other way around.

Security is a critical concern in financial services. According to the 2024 IBM Cost of a Data Breach Report, the average cost of a data breach in the financial services industry was $4.88 million. Custom financial software integrates essential features like multi-factor authentication and data encryption, helping institutions mitigate the risk of data breaches and comply with evolving regulations like GDPR and AML/KYC.

These measures not only secure sensitive financial data but also protect your business from costly breaches and reputational damage.

The fintech market is projected to grow to $917.17 billion by 2032, highlighting the increasing demand for specialized financial solutions. As the number of FinTech users continues to grow, expected to reach 616 million by 2028, custom software becomes essential for financial institutions to meet the rising demand for digital services and personalized experiences.

Custom software is scalable, allowing financial institutions to grow without compromising performance. Whether you need to manage higher transaction volumes or introduce new services like Buy Now Pay Later, custom software not only evolves with your business needs but also integrates seamlessly with cloud platforms.

As Accenture reports, financial institutions effectively utilizing cloud and data see 20–30% productivity gains and a 6% rise in revenue-clear proof that modern architecture drives both scale and cost-efficiency.

Before you begin building, it’s important to consider the factors that can influence long-term success. Here’s what decision-makers need to focus on from the start.

For decision-makers in the BFSI sector, custom financial software development demands a strategic, methodical approach. Ensuring success and scalability depends on understanding key factors at each stage. Here’s what matters most:

Effortless compatibility with legacy systems is essential. Financial institutions often rely on CRM, ERP, or payment platforms, so ensuring smooth interaction between these and your new custom software is crucial. A thoughtful integration strategy minimizes disruption and optimizes operational efficiency.

In financial services, a user-friendly interface isn’t just a luxury; it’s essential for driving adoption and improving productivity. Well-designed systems make everyday tasks quicker and easier, whether for banking, claims management, or investment tracking, directly impacting customer satisfaction and operational efficiency.

Even with the right plan and tools, success depends heavily on who you partner with. These checkpoints will help you choose the right development partner.

Also Read: Building a Successful Financial Platform: Lessons from a $440M Mistake.

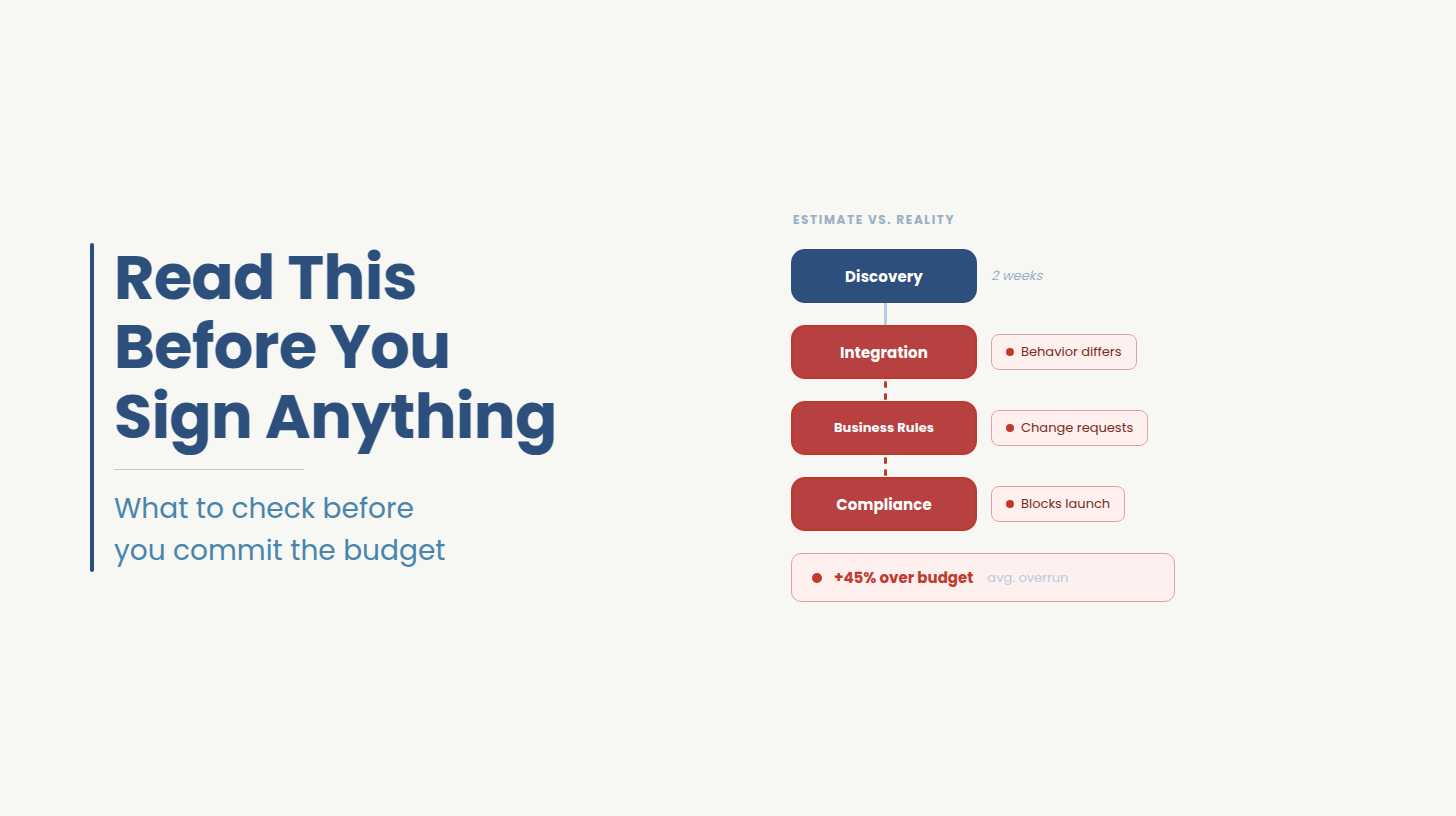

Most BFSI software projects fail because the wrong things got scoped at the start.

There are two ways this happens:

$6.08M is the average cost of a data breach in financial services, 22% above the global average. IBM Cost of a Data Breach Report, 2024. The institutions behind those numbers built the compliance layer on top of the system, in the reporting layer, instead of inside the transaction logic where it belongs. By the time an examiner asked for transaction-level evidence, the fix was a rebuild. Here is where that pattern breaks down in practice.

Here are the three architecture decisions that determine whether a financial software build scales cleanly, survives regulatory scrutiny, or becomes expensive technical debt later.

Most teams build the product first and add compliance tracking in a reporting layer on top. It looks fine during development. It even passes most audits. The problem appears when a regulator asks for transaction-level evidence, and the system can only produce a report without the underlying data trail.

The right approach: Compliance logic embedded inside transaction data flows from the very beginning.

Why it is urgent right now:

If you get this wrong: You are looking at a rebuild instead of a configuration update.

This is the question most institutions forget to ask, until they need to add a new product or switch vendors and find out the answer is "not you."

The right approach: Your institution owns the data model, API contracts are documented and the integration layer can be extended without the original vendor's involvement.

Why this is becoming a regulatory issue too:

If you get this wrong: You discover it 18 months after launch, when every change still has to route through the vendor who built it.

This becomes especially visible in lending environments where institutions outgrow platforms like Encompass but discover their workflows, integrations, and underwriting logic are tightly coupled to vendor-controlled systems. We explored that transition in detail in our guide to custom LOS development after Encompass.

If your financial software uses AI, for credit scoring, fraud detection, onboarding, the model needs to explain every decision it makes.

The right approach: Explainability built into the model pipeline from day one, not added later. Adverse action reason codes generated at the moment of decision, not reconstructed from logs afterward.

What regulators are actually doing:

If you get this wrong: You face active examination exposure and the cost of retrofitting explainability into a model that was never designed for it.

Financial institutions are increasingly discovering that AI governance is an architecture problem. We broke down the governance, explainability, and compliance patterns modern financial institutions are adopting in our guide on AI governance in finance.

Standard platforms handle the basics well. They break down in the same predictable places: institution-specific compliance architecture, complex legacy integration, and AI governance requirements that general-purpose tools were never designed to satisfy.

The categories below are where that breakdown happens. For each one, off-the-shelf platforms consistently fall short on the three architecture decisions this article argues, compliance integration, data ownership, and AI governance. The core components column shows what a correctly scoped custom build must include. The regulations column shows what the build will be examined against.

If your project fits one of these categories, the architecture decisions in the next section determine whether the build holds up long-term.

Every financial software vendor in 2026 will tell you they offer AI. The real question: which of those features will hold up when a regulator looks at them? And which ones will create a problem?

Here is what that looks like across the three most common AI applications in financial software.

Building a credit scoring engine is one thing. Building one that satisfies ECOA's adverse action requirements is a different engineering problem entirely.

What it gives you: Faster, more accurate credit decisions using a wider range of data.

What the build must include:

What gets you into trouble: Using alternative data without documenting why each input variable was chosen. The CFPB's January 2025 Supervisory Highlights show examiners actively searching for less discriminatory alternatives when institutions have not done that analysis themselves.

The institutions seeing the strongest underwriting gains from AI are the ones embedding explainability, governance, and review workflows directly into the scoring pipeline from the beginning. We explored those patterns further in our breakdown of AI in underwriting use cases and ROI.

The architecture question most vendors never raise: what happens when your false positive rate is generating more operational cost than the fraud it is preventing?

What it gives you: Real-time anomaly detection that handles high transaction volumes and evolving fraud patterns.

What the build must include:

What gets you into trouble: A system that catches fraud but cannot produce examination-ready records when a BSA audit asks for them.

There is an important difference between fast KYC and compliant KYC. Both can look the same from the outside. They require different architecture decisions from the start.

What it gives you: Onboarding time cut from multiple days to under an hour, with sanctions screening built into every transaction.

What the build must include:

What gets you into trouble: Every institution that has had to rebuild a KYC system after an examination finding made the same original mistake. They optimized for speed. The compliance documentation was treated as something to sort out later.

Figuring out how to scope a build in a regulated environment? Talk to our financial technology team before you finalize the statement of work. We will identify the compliance gaps and AI governance requirements specific to your project, at no cost.

Choosing the right development service is one of the most important decisions you'll make for your business. A partner who understands your specific needs, regulatory requirements, and technological challenges can drive your project to success. Here's a checklist to help you assess if a partner is the right fit for your custom financial software development needs.

When evaluating a partner, ensure they have deep expertise in the Banking, Financial Services, and Insurance (BFSI) sectors. Financial institutions require custom solutions tailored to their complex workflows, regulatory demands, and operational security needs. Ask yourself:

Compliance is critical in the financial industry. Your software must meet regulations like GDPR, PCI-DSS, and AML/KYC to ensure data protection and regulatory adherence. Check if the partner:

Your business will continue to evolve, and so should your software. It's important to choose a partner who builds scalable solutions. This ensures your system can handle increasing transaction volumes and data without compromising performance. Consider whether the partner:

According to Accenture’s Art of AI Maturity survey, 42% of global C-suite leaders who lead in AI adoption have already seen returns that exceed expectations. The differentiator isn’t just the technology; it’s how strategically and effectively it’s used.

In financial services, AI-driven solutions are no longer experimental. They are central to enhancing decision-making, automating manual processes, detecting fraud early, and delivering personalized customer experiences at scale. The right development partner should not only offer technical AI capabilities but also have the domain understanding to apply them meaningfully in your context.

Here’s what to evaluate:

Software development doesn’t stop at deployment. Ongoing maintenance and support are essential for adapting to evolving business needs and technologies. Choose a partner who:

Effective project management ensures that your software is delivered on schedule and within budget. Before moving forward, ask:

Among the many players in the market, Ideas2IT stands out for a reason. Here’s how our approach delivers meaningful business results.

Most vendors will tell you they have done financial software before. These five questions cut through the sales pitch and tell you if they are the right partner for a regulated environment.

How do you handle compliance requirements that come up in the middle of a build?

A team that has actually worked in regulated financial environments will describe how their architecture is designed to absorb new regulatory requirements without triggering a rebuild. A team that has not will describe their change order process.

Watch out for: Any answer that starts with "we would raise a change order."

Who owns the data model and integration layer when the engagement ends?

There is only one acceptable answer: you do. The data model should be yours. The API contracts should be documented and transferable. The integration layer should be something you can extend without involving the original vendor.

Watch out for: Any hesitation, qualification, or "it depends" on this question.

Tell me about a core banking integration that broke during UAT. What happened?

Every team that has done serious BFSI work has this story. They can name the system, describe what failed, and explain how they fixed it. If a team cannot answer this specifically, they probably have not done enough of this work to know how to prevent it from happening to you.

Watch out for: General answers about integration methodology with no specific incident.

What does your AI governance process look like for a model that makes credit decisions?

The answer should cover: how explainability is architected, how adverse action reason codes are generated, how model drift gets monitored, and how fair lending documentation is produced. It should reference ECOA, Regulation B, and CFPB guidance from 2023 and 2025.

Watch out for: Answers that talk about model accuracy and deployment pipelines but never mention ECOA or the CFPB.

What happens when your client's compliance, security, and product teams disagree on what to build?

In financial software, this happens on almost every engagement. A team that has worked inside enough BFSI organisations has a process for surfacing these conflicts early, before they turn into scope changes that cost three months and a budget overrun.

Watch out for: Describing this as a communication challenge or a project management problem.

Want to put out these questions to our team and run a partner assesment?

Set up a 30-minute partner qualification assessment and we will tell you exactly how we would answer each one for your specific build.

Book a session

We have never believed that billing hours and delivering outcomes are the same thing. That belief is what shaped everything about how Ideas2IT works, the platforms we built, the engineers we deploy, and the model we hold ourselves accountable to.

When an engagement ends, the question we ask is simple: did the software ship, and did the outcome match what was promised at the start? Not whether the hours were billed.

Ideas2IT has spent the last decade building production-grade software for financial institutions across banking, lending, insurance, and fintech with over 500 engagements and a 99% client renewal rate.

Most companies hiring for custom software development are hiring for engineers. What they actually need is the layer that makes engineers maximally effective from day one and that is why we built Anticlock.

What Anticlock changes in a custom software engagement

Week 0: The brief

Traditional: The PM writes a brief but the architect interprets it differently. Finally, the engineers build from a third version that emerged in a standup.

With Anticlock: The brief goes into the Architecture Agent and six hours later, a structured blueprint comes out with feature hierarchy, engineering constraints, tradeoff documentation, and a knowledge graph that every subsequent decision connects to. PM, engineers, and QA start from the same document.

Week 1: Sprint planning

Traditional: Work broken down in Jira from memory, reassembled in tickets, re-explained in standups. Rework on sprint two is almost inevitable.

With Anticlock: The Planner Agent generates codebase-aware work orders with file-level implementation guidance attached. Engineers arrive at sprint one knowing exactly which files to touch and why.

Throughout delivery: Testing

Traditional: Tests are written after features ship because of which coverage becomes inconsistent. And regression risk compounds silently.

With Anticlock: The QA Agent generates 70% of test cases before engineers start every sprint. Coverage grows with the codebase automatically.

Post-launch: Feedback

Traditional: Production issues enter a Jira queue stripped of context. Engineers spend as much time reconstructing context as writing the fix.

With Anticlock: The Feedback Agent maps production signals back into the knowledge graph with full architectural context already attached. Same-sprint resolution.

Here are two ways you can choose to engage with us

Platform-Led Delivery

Our proprietary platforms handle the most expensive phases of every engagement: discovery, analysis, architecture, and test generation. Our engineers work only on the 20 to 30% that requires human judgment. Because each platform is purpose-built for a specific delivery category, teams are not solving the same class of problem from scratch. The result is 40 to 70% faster delivery than a conventional engineering team.

Forward-Deployed Engineering

Our engineers embed inside your organisation as senior team members. They operate on your stack, share your OKRs, and are accountable to delivery outcomes, not hours billed. They bring Ideas2IT's platform tooling with them as an acceleration layer. Domain-matched to your environment. The 99% client renewal rate over 15 years is what happens when engineers own outcomes end to end.

We don’t just talk the talk. We help financial organizations achieve measurable business results through custom fintech software development.

Read the full case study here.

This is one example of how Ideas2IT leverages custom fintech software development services to accelerate product delivery, enhance efficiency, and drive sustainable growth.

But don’t just take our word for it-here’s what some of our clients have to say:

“With just a 2-line Product Vision statement, Ideas2IT developed 3 world-class Open Finance products in under 8 months.”

- Founder & CEO of A venture-backed Fintech platform

By opting for customized solutions, you can ensure that your software is secure, scalable, and aligned with your unique operational needs and compliance requirements. While off-the-shelf software may offer a quick fix, it simply cannot match the flexibility and specific functionality that custom-built solutions provide.

Whether you're focused on improving customer experience, streamlining processes, or ensuring data security, custom financial software equips you with the tools to thrive in the competitive and regulated BFSI sector. Partnering with an experienced development team can make all the difference in shaping the future of your financial operations.

For more information, connect with one of our specialists today.

Didn't find what you were looking for?